Types Of Home Loans

Standard Home Loans

The Standard or Basic Home Loan is the most common type of House Loan.

Can be used to purchase residential property - brand new, under-construction or a pre-owned.

Home Construction Loan

Used to build a house on a piece of own land, instead of buying an existing property.

The bank disburses the loan amount in instalments based on how the construction progresses.

Land or Plot Loan

Empty piece of land with a clear title, can be bought with plot loan.

Borrower is required to construct residential house within 3 years of purchase.

Home Improvement and Extension Loan

To remodel existing property like painting home, fix a leaky ceiling or give property a face-lift.

A Home Extension Loan enables to enlarge home's size by adding rooms, extending floors, etc.

Top-Up Home Loan

The Top-Up Home Loan is one where one can get more finance on existing Home Loan for any purpose.

To remodel house while still repaying your Standard Home Loan or need funds for marriage etc.

Pre-Approved Home Loan

Apply for the loan first and then start looking for a property based on the loan amount eligibility.

Bank determines eligibility based on income. Allows to choose a property that suits repayment capacity.

PMAY Loan

Banks in India (in partnership with the government) offer home loans at subsidised interest rates.

Members of economically weaker sections, light, and medium-income groups are eligible for such a loan.

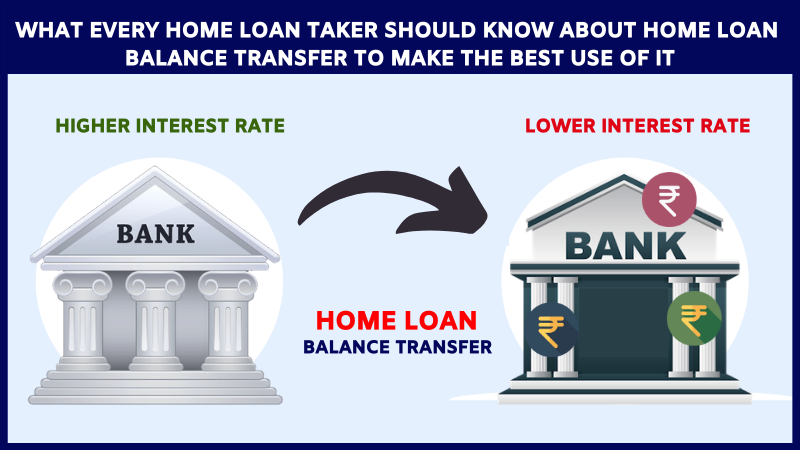

Balance Transfer Home Loan

An existing Home Loan with a bank or NBFC with a high-interest rate, can be transfered to other banks.

Transferring the loan to a bank offering a lower interest rate can reduce your Home Loan's actual cost.

NRI Home Loans

NRIs residing out of the country can easily invest in homes through NRI financing schemes.

Comes at competitive rates with less documentation and based on repayment capacity of the borrower.